This page refers to MedPay in South Carolina.

Since laws differ between states, if you are located in North Carolina, please click here.

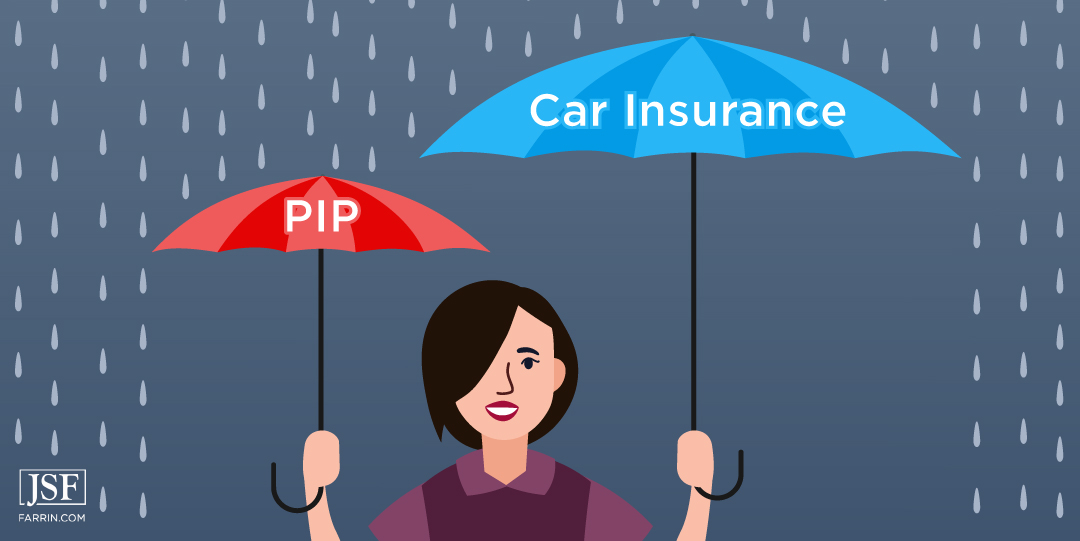

MedPay vs PIP in South Carolina

What’s the difference between MedPay and PIP in South Carolina? There’s a simple answer and a detailed answer – the simple answer being that there isn’t one. The terms are generally used interchangeably, though South Carolina officially uses Personal Injury Protection (PIP). That’s the simple answer, but there is a lot more to know about PIP in South Carolina.

What Exactly is PIP in South Carolina?

PIP stands for Personal Injury Protection. It’s an optional part of your car insurance policy that covers reasonable and necessary medical expenses relating to your injury regardless of who is at fault for the accident that injured you. You can claim it from your insurer no matter who was at fault. While it may not pay all your bills or cover all your expenses, it should give you some relief if you were at fault – and perhaps a bit sooner than the other driver’s liability insurance if you were not at fault.

Is Personal Injury Protection Different Than Bodily Injury Coverage?

Yes, in two important ways.

- Bodily injury liability insurance coverage is a form of liability insurance required by law in the state of South Carolina for all drivers. PIP is optional, not required, and can be purchased from almost any auto insurance company. Both can cover medical expenses caused in an auto accident.

- Bodily injury liability coverage provides coverage depending on who was at fault – the medical bills of a person who was at-fault for the wreck will not be covered by the other party’s liability coverage. PIP covers you regardless of who was at-fault for the wreck, even if you were the at-fault driver.

South Carolina law specifically allows for, but does not mandate, PIP insurance coverage.

Why is PIP Often Called MedPay in South Carolina?

Other states, including North Carolina, refer to similar medical payments coverage as MedPay. You can learn more about MedPay in North Carolina, if you’re curious.

Need personalized help with your PIP claim? Get your case evaluated for free.

Auto Insurance Terminology

Confused by the different names and coverages involved in auto insurance? Here are the facts:

Liability Insurance (required): This is coverage for people who are harmed if you are at fault for an accident. It’s split into bodily injury and property damage portions – the bodily injury portion can cover medical expenses, lost wages, and pain and suffering and would be paid to the other driver and passengers, and the property damage portion covers damage to their vehicle or other property up to the policy limit.

Collision Coverage (optional): This covers your vehicle if you collide with another vehicle or object. If another driver collides with you and causes your damage, their property damage liability insurance generally should ultimately be the one that covers repairs or even replacement cost if your vehicle is totaled, up to the policy’s limit.

Comprehensive Coverage (optional): This protects your vehicle from things not covered under collision coverage, like weather and theft for example, up to the policy’s limit.

Personal Injury Protection (optional): As we’ve explained, this pays your reasonable and necessary medical costs related to an injury regardless of who is at fault for the accident, up to the policy limit.

If I’m Not At-Fault for the Accident, Why Would I Want PIP?

People ask this all the time. If the other driver was at fault, their insurance will pay for my harms and losses and I won’t need PIP, right? Yes and no.

There are a couple of things you should be aware of.

The PIP coverage on your policy may be able to pay you more quickly in some circumstances, and that can be important depending on your situation. There are often delays when it comes to claims against the insurance company for the at-fault driver. Meantime, bills could be piling up. Every circumstance is unique, but PIP can sometimes pay faster.

In addition, if you’ve purchased PIP, you’re paying for it every time you pay your insurance premium. Why would you pay for it if you never intended to use it?

Will Claiming PIP Reduce the Amount of My Compensation From the Liability Insurance Policy?

No. The at-fault driver’s insurance does not get a discount based on your PIP claim. They are separate claims and are treated independently.

Do I Need a Lawyer to Help With My PIP Claim?

The insurance company may make a strong settlement offer quickly, but don’t bet on it. More likely, any offer they make will be quite low. They may stall. They may contest fault. They may even outright deny your claim; every case is different. A lawyer can deal with insurance company pressure on your behalf.

Watch: After My Wreck, What Should I Say to The Insurance Adjuster?

Leveling the Playing Field

This is just one case of many for your adjuster. But the stakes for you couldn’t be higher. Put another way: you’re doing it for the first time and they’re doing it for the fifth time…today.

Many adjusters are trained to identify weak points, and you’re at one of your lowest points after a serious injury. If the adjuster asks you “how you are” and you say “okay, how are you,” that could potentially be used against you. You said you were doing okay after all! If the adjuster asks you how you’re doing and you reveal you’re struggling, they may be motivated to offer you a lowball settlement.

Even if your claim is approved, insurance coverage isn’t a yes or no question. Your claim can be “successful” without you getting the maximum you may have been entitled to. Don’t stress and don’t give in; call us, instead.

Fight for Maximum Compensation With the Law Offices of James Scott Farrin

If you’ve been injured by another driver in an accident, you’re fortunate to have opted for PIP coverage. It can be helpful in times of need – but you should seek fair compensation from the at-fault driver’s policies to address the harm done to you and the losses you’ve suffered.

In addition, while there may be multiple policies against which you can claim, insurance policies have limits. In other words, if your claim exceeds the policy’s limit, you’ll have to find other means of potential compensation. You want an attorney in your corner who knows the law and how to seek the compensation you may deserve from the right sources.

The James Scott Farrin Advantage

Since 1997, we’ve recovered over $1.8 billion in total compensation for more than 65,000 clients. And counting.1

Picking the firm to fight for you is a critical decision. Here are two more benefits of choosing the James Scott Farrin Advantage:

Speed: Our proprietary, patented software and optimized workflows have earned national recognition.

Risk-Free Payment Arrangement: No Attorney’s Fee Unless We Recover for You2

![]() Put your trust in us. We were named a 2024 “Best Law Firm” by U.S. News – Best Lawyers. Firms included in the “Best Law Firms” list are recognized for professional excellence with persistently impressive ratings from clients and peers.4

Put your trust in us. We were named a 2024 “Best Law Firm” by U.S. News – Best Lawyers. Firms included in the “Best Law Firms” list are recognized for professional excellence with persistently impressive ratings from clients and peers.4

Call us right now at 1-866-900-7078 or contact us online for a free case evaluation. Don’t delay a moment longer – tell them you mean business!