I’ve seen it happen to too many clients. One moment, they’re driving through Greensboro — heading home on I-40 after work or running errands near Friendly Center. The next moment, another vehicle slams into them, and before they can process what happened, the other driver speeds away. They’re left sitting at the scene, shaken and hurt, with no idea who just changed their life.

Hit-and-run accidents in Greensboro are frighteningly common, and I can tell you from experience that Greensboro drivers face particularly high risks. The city consistently tops the North Carolina Department of Transportation crash list.

When I sit down with clients who’ve been through this, one of the first things they tell me is that they first assumed there was no way to recover compensation since the driver who hit them disappeared. I understand why they feel that way, but here’s what I always want people to know: your own auto insurance policy likely contains coverage specifically designed for this kind of situation.

Key Takeaways About Greensboro, NC Hit-and-Run Accidents

- Hit-and-run accidents are treated as uninsured motorist claims under North Carolina law, which might allow injured people to seek compensation through their own insurance policies.

- North Carolina law (G.S. 20-279.21) requires insurance coverage for uninsured and underinsured motorists on all auto policies.

- To file an uninsured motorist claim after a hit-and-run, the unidentified vehicle must have made physical contact with your vehicle, and the accident must be reported to authorities within 24 hours.

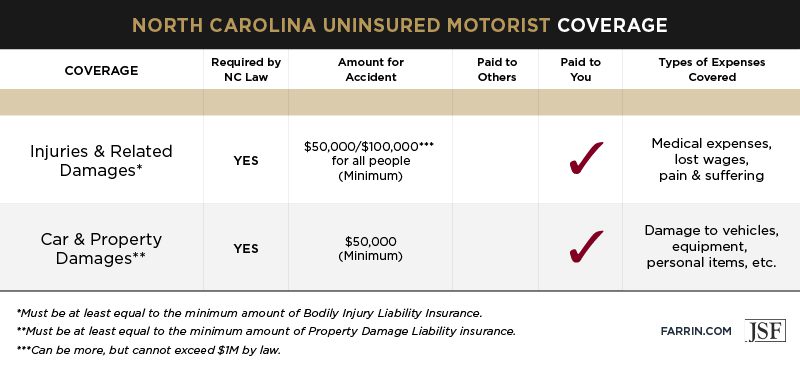

- As of July 1, 2025, North Carolina raised minimum liability and uninsured motorist coverage limits to $50,000 per person and $100,000 per accident.

- Working with an experienced car accident attorney can significantly increase the odds of a successful claim outcome.

Understanding Hit-and-Run Accidents in Greensboro, NC

Greensboro’s unique road system creates conditions where hit-and-run accidents happen with troubling frequency. The city hosts several major highways, including the Greensboro Urban Loop that carries I-73, I-85, I-785, I-840, and US 421 all within city limits. Crash hotspots include Interstate 40 exchanges at Randleman Road, Elm-Eugene Street, and Martin Luther King Jr. Drive, where narrowing lanes create a dangerous mix of congested traffic and drivers traveling at highway speeds.

A hit-and-run happens when a driver involved in a collision leaves the scene without stopping to provide information or offer assistance. This applies to all kinds of collisions, from serious accidents with injuries to minor scrapes in parking lots.

Under North Carolina law, drivers who flee the scene can face significant criminal penalties, including financial penalties and jail time. But criminal charges against the fleeing driver — if they’re ever caught — don’t put money in your pocket for medical bills and lost wages. That’s where your potential insurance coverage becomes essential.

How Uninsured Motorist Coverage Applies to Hit-and-Runs

Under North Carolina law, a hit-and-run driver is classified the same as an uninsured driver for insurance purposes. North Carolina General Statute 20-279.21 requires every bodily injury liability insurance policy to provide protection for persons insured who are legally eligible to recover damages from owners or operators of “uninsured motor vehicles and hit-and-run motor vehicles.”

This means your uninsured motorist (UM) coverage can potentially help pay for your injuries, medical treatment, lost wages, and pain and suffering — even when the at-fault driver disappears.

What Uninsured Motorist Coverage Typically Pays For

When you file a UM claim after a hit-and-run, your policy might help compensate you for various types of harm, such as:

- Medical expenses: Emergency room visits, surgeries, hospital stays, physical therapy, prescription medications, and ongoing treatment

- Lost wages: Income you may miss while recovering from your injuries, including potential future earning capacity if you’re left with permanent limitations

- Pain and suffering: Physical pain, emotional distress, and reduced quality of life resulting from the accident and your injuries

- Travel expenses: Mileage or rideshare costs (must show receipts/proof)

The amount you might recover depends on your policy limits and the severity of your injuries.

Recent Changes to Auto Coverage Limits

North Carolina recently made significant updates to auto insurance requirements that could affect your claim. Starting July 1, 2025, for all new or renewed policies:

- The minimum insurance limits for bodily injury liability insurance and uninsured motorist (UM) insurance increased to $50,000 per person and $100,000 per accident.

- The minimum insurance limit for property damage increased to $50,000 for both liability and uninsured motorist.

The July 2025 changes also abolished the “credit rule” for liability insurance payments. Previously, North Carolina allowed underinsured motorist carriers to receive a “liability setoff” from payments made by the liability carrier. The new law eliminates this setoff, meaning injured people can potentially collect more total compensation when combining coverage from multiple sources.

Critical Requirements for Filing a Hit-and-Run Claim

Successfully recovering compensation after a hit-and-run involves meeting specific legal requirements. Missing any of these steps could jeopardize your claim.

The Physical Contact Rule

For a hit-and-run uninsured motorist claim to succeed, the unidentified vehicle must have actually made physical contact with your vehicle. In single-vehicle accidents where there’s no physical contact with another vehicle, your UM claim might be denied unless there is strong evidence showing another driver was involved and responsible for forcing you off the road.

This physical contact requirement exists to prevent fraud. It means that if another driver cuts you off and causes you to crash without actually hitting your vehicle, pursuing a UM claim becomes significantly more difficult — though not impossible with strong witness testimony and other evidence.

The 24-Hour Reporting Requirement

The accident must be reported to the authorities within 24 hours, or as soon as possible thereafter. This requirement is built into North Carolina law and insurance policies. Failing to promptly report the hit-and-run to police can give your insurance company grounds to deny your claim.

Prompt Insurance Notification

Your insurance company must be promptly notified of your injuries, losses, and other details about the accident. Don’t wait weeks or months to contact your insurer — doing so could raise red flags and complicate your claim.

Common Challenges With Hit-and-Run Claims

Filing a claim against your own insurance company for uninsured motorist benefits isn’t the same as filing against another driver’s insurer. While it’s your policy, your insurance company likely has financial incentives to minimize payouts.

Proving Fault Without the Other Driver

Insurance companies typically require claimants to prove they are legally eligible to damages. Filing an uninsured motorist claim is not the same process as filing a personal injury lawsuit in civil court; nonetheless, insurance companies often require claimants to prove that the uninsured driver was at fault and caused their injuries.

Without the other driver present, you’ll need to build your case through evidence such as:

- Police reports documenting the accident

- Witness statements from people who saw the collision

- Physical evidence like vehicle damage patterns and debris

- Surveillance footage from nearby businesses or traffic cameras

- Your own documentation from the scene

Disputes Over Injuries and Compensation

Even when fault isn’t disputed, insurance companies might challenge the severity of your injuries or the amount of compensation you’re requesting. They might argue that some of your medical treatment was unnecessary, that you had pre-existing conditions, or that your injuries aren’t as severe as your doctors indicate.

This is where having a Greensboro car accident attorney who fights for injured people can make a real difference. An experienced car accident lawyer knows how to build compelling cases, work with medical professionals as needed to document injuries thoroughly, and push back against lowball settlement offers.

Who Is Covered Under Your Policy?

Your uninsured motorist coverage typically extends beyond just you. Coverage is generally available to the policyholders named on the policy, the named insured’s spouse and relatives residing in the same household, any person using or riding in a vehicle insured under the policy with consent of the named insured, and any other person lawfully possessing an automobile insured under the policy.

This means that if a family member is driving your car when a hit-and-run happens, or if you’re injured as a passenger in someone else’s vehicle, there might still be coverage available to you. Understanding who qualifies for coverage under your policy is an important step in determining your options.

The Statute of Limitations for Hit-and-Run Claims

Time limits apply to pursuing compensation after any car accident. Personal injury claims must generally be filed within three years from the accident date under North Carolina’s statute of limitations laws. While three years might seem like plenty of time, building a strong case, gathering evidence, negotiating with insurance companies, and potentially preparing for litigation takes longer than most people expect.

Starting early matters. Witnesses forget details, surveillance footage gets deleted, and physical evidence disappears. You should begin working on your claim immediately.

Hit-and-Run Accidents in Greensboro FAQs

Here are answers to some common questions people have after being injured in a hit-and-run collision.